CVS Employee Stock Purchase Plan: A Complete Guide to Smart Participation

The CVS employee stock purchase plan (ESPP) is a powerful tool designed to help CVS Health employees build long-term financial security. By offering company stock at a discounted price through payroll deductions, the CVS stock purchase plan provides an immediate return on investment while encouraging employee ownership. In this guide, we explain how to enroll, optimize contributions, and align your strategy with broader financial goals.

CVS ESPP is like getting a risk-managed bonus every quarter. For disciplined savers, it's the most predictable ROI in personal finance. — Chris Kawashima, CFP, Fidelity Investments

Understanding the CVS Employee Stock Purchase Plan

What is the CVS ESPP?

The cvs employee stock purchase plan allows eligible employees to buy CVS Health stock at a 15% discount, with purchases occurring quarterly. Employees can contribute between 1–10% of their base salary, up to the IRS limit of $25,000 annually. Thanks to a look-back provision, the purchase price is set at the lower of the stock’s value at the beginning or end of the offering period—potentially increasing the effective discount beyond 15%.

This stock purchase mechanism not only supports employee ownership but also aligns interests with CVS Health’s long-term success in the health care sector. Each offering period typically runs for a full month period, concluding on the last business day of the quarter.

"The look-back feature during volatile quarters has pushed effective discounts as high as 32%. That’s a phenomenal buffer against market drops." — Melody Kazel, financial analyst at Investopedia

Who Is Eligible and How to Enroll

To participate, you must be employed by CVS Health or a qualifying designated subsidiary and meet specific service criteria. Enrollment is completed via the company's HR portal during the designated CVS ESPP enrollment period before each quarterly purchase date. For login details and support, check the CVS employee stock purchase plan login or access the CVS employee stock purchase plan PDF from your HR dashboard.

| Offering periods end: | March 31, June 30, September 30, December 31 |

| Max contribution: | $2,083/month (depending on base pay expectation for CVS) |

| Plan contact: | See the CVS employee stock purchase plan phone number in internal resources |

| Note: | Contributions are made via payroll deductions and may be adjusted each pay period. |

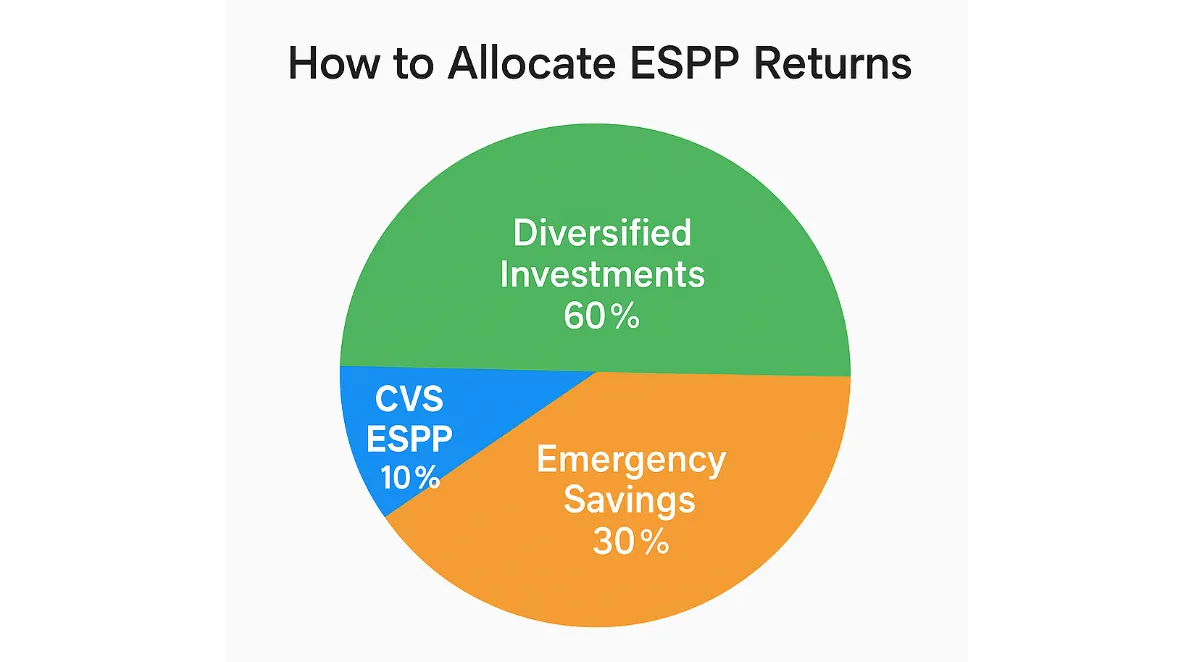

Smart Contribution Strategies and Financial Integration

Maximize Guaranteed Returns

The CVS ESPP offers an immediate 17.65% ROI when you buy $100 worth of stock for $85. For most employees, especially those who have already taken advantage of their CVS employee 401k match, contributing the maximum to the ESPP provides unmatched returns versus traditional options like 401(k)s, index funds, or high-yield savings accounts.

| CVS ESPP (with discount): | 17.65%+ potential growth |

| S&P 500 Index: | 10–11% historical average |

| CVS 401k Plan (with match): | ~50–100% on contributions, investment-dependent |

The stock plan is designed to be a way to save consistently toward financial goals, especially when combined with a savings account.

Balance Flexibility with Growth

A liquidity-balanced strategy helps maintain cash flow:

- Contribute 4–6% of salary

- Sell 70–80% of stock each quarter to recapture capital

- Reinvest proceeds in diversified funds while keeping 1–2% in CVS shares

- Maintain emergency savings (3–6 months of expenses)

This method positions the CVS stock options employees receive as a repeatable income stream while reducing concentration risk.

You may elect to contribute less in months with high expense forecasts, and may sell shares to meet short-term needs.

Managing Risk and Taxes Effectively

Tax-Efficient Selling

- Immediate sale: Discount taxed as income; additional gain taxed short-term

- 1–2 years hold: Gain taxed at long-term capital gains rates (15–20%)

- Rolling sale strategy: Blend immediate and delayed selling to balance liquidity with tax efficiency

You can track your CVS ESPP purchase date and identify lots nearing tax-advantaged status using brokerage platforms that provide tax lot tracking and Form 3922 support. After-tx planning is essential for optimizing your real return.

Avoiding Overconcentration

If CVS stock exceeds 10–15% of your portfolio, implement a core-satellite model:

- 70–80% core in diversified ETFs/index funds

- 5–15% satellite in CVS shares

- Rebalance quarterly using ESPP proceeds

CVS employee stock purchase plan reviews highlight that disciplined reallocation significantly reduces risk exposure while preserving long-term gains.

Enhancing Financial Wellness with ESPP

Dividend Reinvestment and Long-Term Growth

ESPP participants can use dividend reinvestment to increase their holdings over time. When CVS Health pays dividends, they can be automatically used to buy additional shares, enhancing accumulate potential.

This compounding strategy can lead to exponential portfolio growth, especially when combined with quarterly contributions.

Long-Term Planning and Retirement

Use the ESPP CVS as part of a broader retirement strategy:

- Align contribution level with career stage and financial goals

- Review allocation quarterly

- Coordinate with CVS 401k plan to maximize tax advantages

You can also use the ESPP to build wealth in preparation for large life events or as a complement to brokerage accounts. Shares held longer also improve tax treatment upon disposition.

"Holding shares for tax-qualified disposition changed everything. I saved nearly $2,000 in taxes in one year." — Marc, active ESPP participant

Practical Next Steps to Maximize Your ESPP

- ✅ Enroll now during the CVS ESPP enrollment period — set payroll deductions.

- 📅 Mark your calendar for the offering period and CVS ESPP purchase date.

- 💼 Track your tax lots using qualified brokerage accounts that support Form 3922 and detailed tax lot tracking — such as Fidelity, Charles Schwab, or TD Ameritrade. These platforms allow you to monitor ESPP shares by purchase date and offering period, helping you time sales for maximum tax efficiency.

- 🔁 Rebalance quarterly — cap CVS holdings at 10‑15% of your portfolio; redirect proceeds to index funds.

- 📚 Educate yourself — check the CVS employee stock purchase plan PDF for plan details, or call the CVS employee stock purchase plan phone number.

One of the most overlooked CVS employee stock purchase plan benefits is the ability to generate immediate returns through a built-in 15% discount on stock purchases.

Quick Start: Trade Stocks with Pocket Option

Want to start trading stocks right now without waiting for an offering period or payroll deductions? Pocket Option allows you to trade leading company shares instantly through Quick Trading.

Why Trade Stocks on Pocket Option?

- 🚀 Start with a minimum deposit from $5

- ⏱️ Instant market access with just two buttons: Buy if you expect the price to rise, or Sell if you predict a drop

- 📱 Available on mobile and desktop with fast, intuitive interface

- 🔍 Trade popular stocks with real-time market data and customizable charting tools

You don’t need to wait for quarterly ESPP windows—just sign up, fund your account, and begin trading shares immediately. It’s a great way to explore stock market strategies while building financial discipline.

Unlocking the Full Potential of the CVS Stock Purchase Plan

The CVS employee stock purchase plan offers more than discounted shares—it’s a strategic asset. Whether you’re aiming to build wealth, reduce debt, or plan for retirement, thoughtful participation in the CVS ESPP can elevate your financial wellness.

Checklist for Success:

- Enroll on time via CVS ESPP login portal

- Start with at least 5% contribution

- Monitor stock price performance and rebalance regularly

- Understand tax implications before selling

- Diversify investments to protect long-term security

For more information, access the CVS employee stock purchase plan PDF or contact support via the CVS employee stock purchase plan phone number provided by HR.

Keep in mind: your shares acquired during each offering are subject to plan rules. You may amend your deduction choices at each new period, and the plan is administered with compliance to IRS regulation for qualified plans. Understanding your eligibility and contribution limits ensures the plan qualifies you for the best possible outcome.

Finally, be sure to track the day of the offering period and plan when to sell shares based on market conditions, investment goals, and tax planning. This disciplined approach will secure your security and long-term wealth growth. Discuss this and other topics in our community!

Zobacz więcej:stockstrategyinvestmentInterestingTrading Strategies